Student loans are quickly becoming the next major crisis facing the American economy. There are several ways they can cripple your ability to get ahead financially. Large student loan debt often stands in the way of buying a home, car, or investing for your future. Another sad consequence is many Americans are afraid or unable to start a family out of fear of not being able to provide due to crushing debt. The reality is that money is very important for many things in life and debt makes it a lot harder to accrue wealth.

America’s outstanding student loan balance is projected to surpass to two trillion dollars by 2022. The consensus from most experts is that a large portion of it is unlikely to ever be repaid given the fact that nearly a quarter of student loan borrowers are currently in a state of delinquency or default. This is crazy when you think about this. Two trillion dollars???

So, what’s the best way to get rid of student loan debt? Depending on who you ask you’ll get a variety of answers. Some advisors will say to defer them. Others will recommend working in public service for 10 years with the hope of qualifying for loan forgiveness.Finally, there’s the income-based repayment crowd who are essentially recommending a lifetime of dealing with student loan debt.

Obviously, the best way to get rid of student loans is to not have them in the first place. But you probably wouldn’t be reading this if that were the case, and let’s be real, most of us don’t have a wealthy spinster aunt who just wants to pay for your education.

Quick Answer For Getting Rid of Student Loan Debt

The best way to get rid of student loan debt is to focus on maximizing and increasing your productivity. Deferment, Debt Consolidation, Public Service Loan Forgiveness (PSLF) and income-based repayment are all band aids that don’t ultimately address the real problem. Based on current laws, the only guaranteed way out of student loans is to pay them off. So, direct your focus towards increasing your income which comes from increasing your productivity. Use every extra dollar that comes into your hands to pay down the debt.

There you go. That’s the quick answer that I promise will work 100% of the time. It will work for both publicly funded and private student loans. But just so you don’t have to take my word for it, let’s dig into some of the common recommendations and show why they’re collectively a bad idea.

The best way to get rid of student loan debt is to focus on maximizing and increasing your productivity.

Ron Henry Click to Tweet

Deferring Student Loans

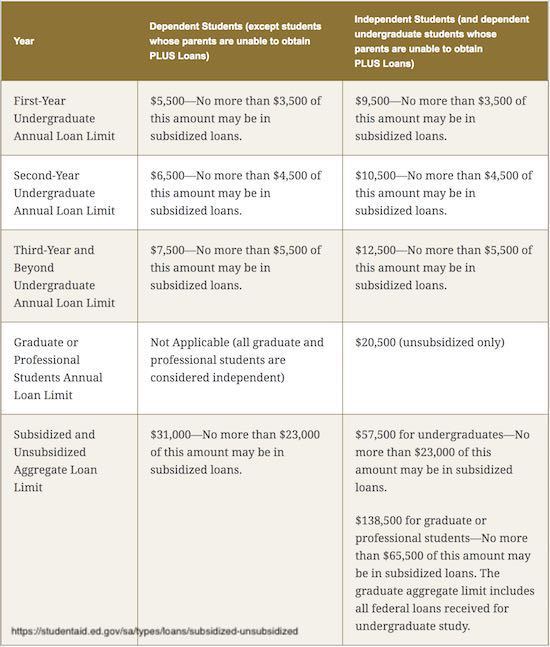

Unless you’re currently in school and unable to work, you’ll probably want to avoid deferring student loan payments. Unless your loan is subsidized by the federal government, interest will continue to accrue even though you’re not making payments.

For most borrowers, only a small percentage of their student loan is subsidized. The current total cap for subsidized student loans is $23,000. This regardless of whether you’re a dependent student (getting assistance from your parents or family) or an independent student (paying for it all yourself).

What this means is that most student loan balances are increasing while in deferment. That’s the wrong direction. Ultimately the loan has to be repaid, so it’s best to get on with doing that as soon as possible.

As a reference, I’ve attached the following chart which shows the current 2018 /2019 aggregate limits for subsidized and unsubsidized student loans.

Public Service Loan Forgiveness Largely Doesn’t Work

The Public Service Loan Forgiveness (PSLF) Program was established by Congress with the passage of the College Cost Reduction and Access Act of 2007. It was created to encourage individuals to enter lower-paying but vitally important public sector jobs such as military service, law enforcement, public education, and public health professions.

In theory the PSLF Program allows eligible borrowers to qualify for forgiveness of the remaining balance of their Federal Direct Loan (Direct Loan) Program loans after they have served full time at a public service organization for at least 10 years, while making 120 qualifying payments.

The reason why I say “in theory” is that there are several ways to become disqualified. If you make a payment too early or too late, it won’t count towards the 120 required. Work less than an average of 30 hours per week over the course of a year and you’ll be unlikely to qualify. There are several other “gotchas” that will cause you to be rejected when you apply for forgiveness. Here are nine I found while doing the research for this article.

9 Ways to Be Rejected for Public Service Loan Forgiveness

Failing to enroll in an income-based repayment plan

Not getting your employment certification form endorsed by your employer

Not consolidating Perkins or Federal Family Education Loans (FFEL) Loans to a Direct student loan

Submitting an incomplete or error filled Employment Certification Form

Thinking Public Service Loan Forgiveness is automatic

Skipping student loan payments

Thinking that your job is the qualifying factor when it’s really your employer

Not making use of Temporary Expanded Public Service Loan Forgiveness

Failing to re-certify your income every year

Missing any one of these can result in your PSLF application being rejected – which seriously hurts your chances at loan forgiveness. By not meeting the requirements, you’re now 10 years down the road and still on the hook for the entire remaining balance.

Also, in the highly unlikely event that you are approved loan forgiveness, the amount forgiven could be treated as taxable income for that year. For example, let’s say you had $50,000 in student loan debt. If you managed to meet all the requirements for loan forgiveness, the IRS could add the $50,000 in forgiveness money to your income for that calendar year. For most people the result is going to be a rather large tax bill.

Even though the laws around PSLF don’t currently treat the forgiven amount as taxable income, there’s nothing that says the IRS couldn’t modify this in the future. In the most recent budget, there’s already been a precedent set for making changes to the PSLF program. As more people attempt to make use of PSLF, modifying the way the forgiven money is treated for tax purposes could very well become a reality.

What Are Your Odds?

If you want additional evidence that PSLF is a bad bet, take a look at a recent report from the U.S Department of Education. The report showed that only 96 out of 29,000 applications for loan forgiveness were approved. Let me put that in perspective for you. The federal government rejected 99.7% of loan forgiveness applications. That reads a lot like pretty much all of them.

Imagine the feeling of rejection after working for 10 years in a low-paying public sector job because you were banking on loan forgiveness. Also consider that people going this route are likely on income-based repayment. That usually means that the principal of the loan hasn’t seen a major reduction in the 10-year period.

Also realize that there’s no guarantee that the forgiveness program will be around in the future. Depending on the administration in power, priorities tend to shift. The most recent federal budget extends repayment before forgiveness to 15 or 30 years depending on if you borrowed for an undergrad or graduate degree.

Here’s the direct quote from the budget document:

“For undergraduate borrowers, any balance remaining after 15 years of repayment would be forgiven. For borrowers with any graduate debt, any balance remaining after 30 years of repayment would be forgiven.”

Does 15 to 30 years of bondage at below-market wages sound like a good financial plan to you? It doesn’t to me.

Does 15 to 30 years of bondage at below-market wages sound like a good financial plan to you?

Ron Henry Click to Tweet

Using Your 401k To Pay Off Student Loan Debt

Is cashing out your 401k to pay off student loan debt a good idea? The short answer is no. Any money withdrawn will be taxed at your ordinary income rate. If you’re younger than 59 ½ (which is probably true for most with student loans), you will also pay a 10% early-withdrawal penalty. This is incredibly damaging to your finances.

Just so the math is easy, let’s assume you have 401k balance of $100,000. Let’s also assume that between your federal and state income tax rate, you pay 30% of your salary to the IRS and state government.

If you decide to cash out your 401k to pay student loan debt, you’ll give up a total of 40% of your 401k balance in taxes and penalties. You’ll have turned that $100,000 into $60,000. There’s no way that you student loan interest rate isn’t high enough to offset losing 40% of your money. Don’t forget that by withdrawing money from your 401k, you’re also seriously damaging your retirement nest egg. It’s simply not worth it.

A Better Way

Instead of focusing on the least painful way to get rid of student loan debt, focus on the most effective way.

Take a “rip the band aid off quickly” approach to student loan debt repayment. You’ll get rid of the loans faster that way. It’ll enable you to get on with your life instead of wasting 10 years or more hoping for a government life line.

Ways to Maximize and Improve Your Productivity

Hopefully I convinced you that relying on loan forgiveness is likely to be a losing strategy. Since we’ve established that the best way to get out of student loan debt is to pay it off, let’s look at some ways to improve your productivity.

I’ll give you a list of 7 that I really like.

1. Eliminate Time Wasters

TV, social media, extraneous Internet surfing can be huge time sucks. Paying off student loans takes money and at this stage of the game making money is going to require time. Get rid or seriously reduce any activities that don’t contribute towards your ability to eliminate the debt.

2. Get Better at Your Profession

Everyone has the ability to do better in their current job. If you upgrade your skills through seminars, reading, and inexpensive courses, you can quickly become much better at what you do. Your employer is likely to take notice of this which will increase your economic value to the organization. The more valuable you are, the more they’re likely to pay you.

3. Work Extra Hours at Your Current Job

If you’re paid hourly, ask about working additional hours. It doesn’t hurt to ask. Even if they say “no” you’re really no worse off than you currently are. You already have track record with your current employer so it makes sense start there when looking for opportunities to increase your earning power.

4. Pick Up an Extra Job

If you’re salaried or there aren’t any immediate ways to increase your income at your current job, consider picking up a side hustle. You could drive for Uber / Lyft, deliver pizzas, or wait tables. Those three options came to mind because the hours tend to be more flexible. Their inherent flexibility makes it easier to blend them in with your primary job without causing too much disruption.

5. Networking

Most people have their current job because of someone they know. Leverage your professional network as a means to find new opportunities. Who you know and who they know can give you a leg up on changing jobs or finding side work.

6. Start an Online Business

Entrepreneurship is a great option for serving others while also increasing your income. Online businesses like a blog can generate great income, but they do take a while to get going. If you decide to go this route, I recommend doing this in addition to tip number 4 (Pick up an extra job). Having an extra job will give you more income now to throw at your student loan debt.

Building an online business is a great idea, but it’s more of a long-term play.

7. Minimize Your Expenses

With all the hard work you’re doing to increase your income, let’s ensure it’s not consumed by unnecessary expenses. Small recurring expenses do add up, so you’ll want to do all you can to minimize them. Immediately after college isn’t the time to drastically inflate your lifestyle under the assumption that you can always pay for it later. Your loans should be first priority.

401k Match for Student Loan Debt Repayment

In August of 2017, a private company asked the IRS to allow them to contribute 5% of the worker’s salary to their 401k plan as long as the worker paid at least 2% of their income towards student loan debt. The company no doubt made this request out of concern that their employees weren’t saving anything for retirement due to being saddled with student loan repayment.

The verbiage directly from the IRS letter reads as follows:

“Under the program, if an employee makes a student loan repayment during a pay period equal to at least 2% of the employee’s eligible compensation for the pay period, then Taxpayer will make an SLR nonelective contribution as soon as practicable after the end of the year equal to 5% of the employee’s eligible compensation for that pay period.”

“Taxpayer” in the statement refers to the company.

How the Plan Works

In a nutshell, as long as the employee provides evidence that they are paying at least 2% of their salary towards student loan debt, the company will make a matching 401k contribution equal to 5% of their salary. What’s especially nice about this is the employee isn’t required to actively contribute to their 401k in order to receive the benefit.

It’s an interesting concept that could be a great option for getting rid of your student loan debt while still saving for retirement. Before you get too excited, realize that this plan currently only applies to a single corporation. The letter doesn’t say who the company is. If the program sounds appealing to you, it might be worth bringing up to your company’s 401k plan sponsor.

If there’s enough demand, the IRS may very will consider allowing widespread adoption of the program. Can’t hurt to try.

It’s a Marathon not Race

On the slim chance that you are reading this prior to taking on student debt, I hope that this has given you a moment to think. Really scrutinize whether you really need a college an education paid for with debt to do your selected profession. There are other avenues for education that don’t require college or massive student loan debt. Being realistic and practical can save you lots of money and stress.

It’s important to realize that getting rid of your student loan debt by paying it off will take time. You didn’t create all the debt in a month so it’s not realistic to think that you can get rid of it immediately.

You didn’t create all the debt in a month so it’s not realistic to think that you can get rid of it immediately.

Ron henry Click to Tweet

When you feel down because of your situation, try shifting your focus to what you’re gaining by paying off the debt. You’re getting freedom of choice back. Once student loan debt is gone you open up a ton of options in your life.

Money will no longer have to be the determining factor when choosing where to work. You’ll eliminate stress in places you didn’t even know you had. It’s definitely not easy. It’s just worth it.

If you have any other ideas for getting rid of student loan debt, let me know in the comments below!

Legal Disclaimer: The information provided and accompanying material is for informational purposes only. It should not be considered legal or financial advice. You should consult with an attorney, CPA or other professional to determine what may be best for your individual needs.