If you were to survey a random group and pose a question of how much they needed to save for retirement, you’d likely be greeted with blank stares. If you posed the same question to most financial planners or performed an online search, the general answer you’d likely receive is “10% of your income over several decades”. What do you think? Is the conventional recommendation of a “10% personal savings rate” good advice? I don’t. Let’s dig into why.

Assumptions

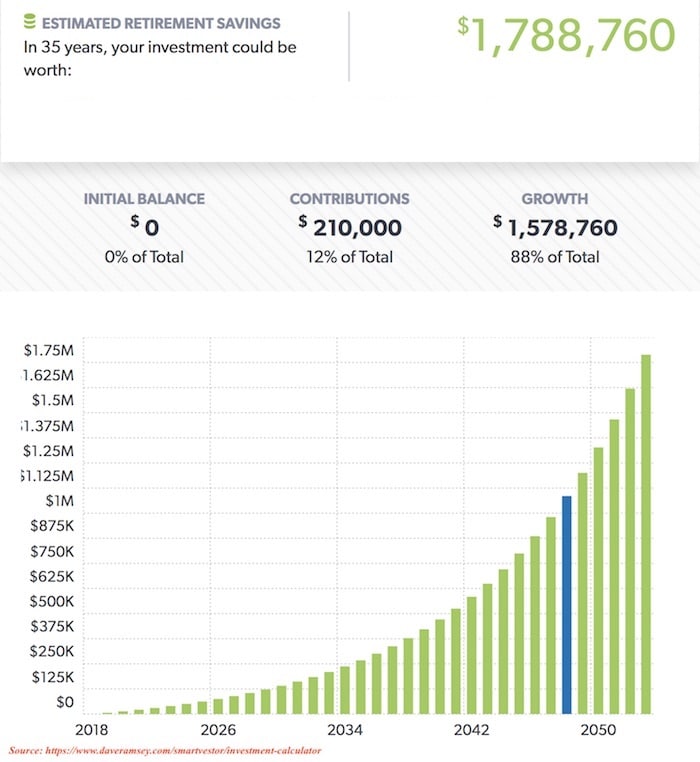

Let’s use the example of a couple (we’ll call them Alice and Bob) earning an average combined income of $60,000 per year. 10% of 60k is $6,000 per year or $500 per month. We’ll also assume an annual market return of 10%. The couple makes the decision to invest $500 per month from age 30 to age 65. If we run those parameters through an investment calculator we come up with a grand total of $1,788,760 or approximately 1.8 million dollars

Not shabby but also not very impressive when you consider it took 35 years to amass that sum of money. You’re probably thinking I’m crazy for having this opinion but hear me out.

Time is more valuable than money

Unknown Click to Tweet

Time is More Valuable Than Money

It took Alice and Bob 35 years to amass their fortune. That’s a long time to wait for some semblance of financial independence. Over that time period, they probably had kids, sent them to college and may even have a grandchild or two. They worked for over three decades and only ended up with $1.8 million. Also consider that they don’t get to keep all $1.8 million. Unless they’ve built a money machine using a dividend growth strategy, every time they sell some of their stock, they’ll realize a potentially large tax bill.

There’s also nothing that says that both Bob and Alice will want to remain in the job market for the 35 years required to amass the $1.8 million. As we grow older it’s not uncommon for our priorities to change. This makes it unwise to undertake a financial retirement strategy that requires a 35-year commitment.

Inflation

$1.8 million sounds like a lot until you consider the nasty little element of inflation. Inflation slowly erodes the buying power of money over a period time. Remember when you could buy a gallon of gas for less than a dollar? It was a over 20 years ago at this point. That’s an example of inflation we feel every day.

Back to Alice and Bob. Given inflation, what will it take to have $1.8 million worth of buying power in 35 years? If we use a conservative inflation rate of 2.1%, they would need $3,402,242 in 35 years to equal the buying power of $1.8 million today. Stated another way, in 35 years their $1.8 million is going to be worth the equivalent of $864,273 in today’s dollars. That doesn’t leave very much room for error.

$1.8 million sounds like a lot until you consider the nasty little element of inflation.

Ron Henry Click to Tweet

A Better Way

If we could get Alice and Bob to commit to a total savings rate of 35%, they end up in a much better situation. It leaves them 65% of their income to use for living expenses and entertainment. We’ll divide the 35% into 3 major buckets.

Bucket 1 – Emergencies

5% will initially fund their “life happens” bucket. It’s also referred to as an emergency fund and is used for well… emergencies. Unexpected medical issues, home repairs, car breakdowns, etc. Ideally the value of this bucket should represent 3 – 6 months of living expenses. How large you make this bucket is very much a personal decision but it should be large enough to prevent you from having to touch your investment funds.

Bucket 2 – Large Purchases and Opportunities

With bucket 1 fully funded, Alice and Bob, would divert the 5% they used to build their emergency fund to now start filling the large purchases / opportunity (LPO) bucket. The use of LPO cash is somewhat flexible. It can fund the purchase of big-ticket items like replacing a car or taking a nice vacation. Alternatively, it can be used to take advantage of new investment opportunities that may arise. This bucket allows them to live a life of fulfillment while still building their future nest egg.

Bucket 3 – Regular Investments

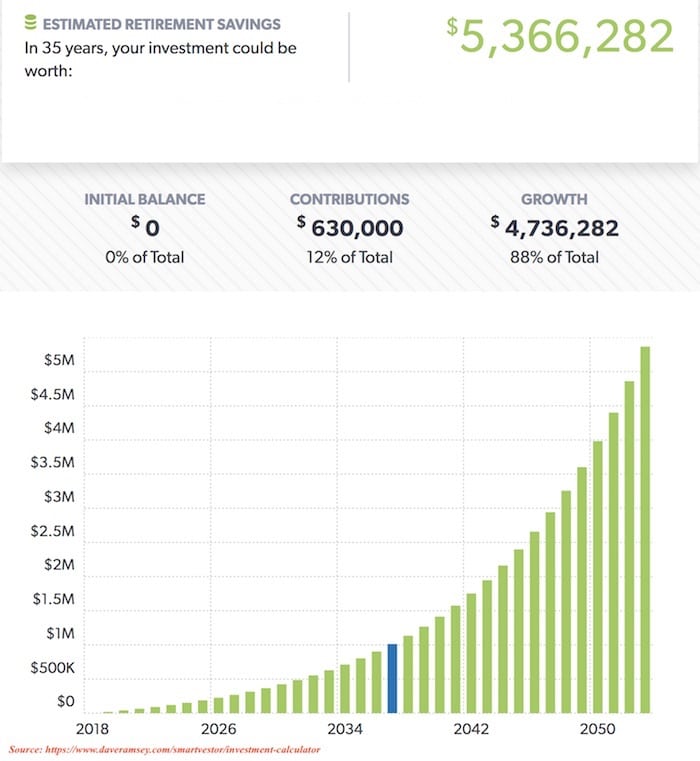

This is the bucket we use for building wealth. If we take 30% of Alice and Bob’s $60,000 salary we come up of with $18,000 or $1,500 per month. When we run that through the investment calculator with the same parameters (35 years at 10% compounded annually), $5,366,282 emerges.

Now we’re talking. This number more than compensates for inflation and provides a nice cushion. Alice and Bob can even live a more materially-rich life if they choose to. They have additional money to help family members and friends. It allows them to be more generous with their charitable donations. Going from a 10% to 35% personal savings rate made tremendous difference. If their goal was $1.8 million, they would reach it 11 years sooner by the increase in personal savings rate. Alice and Bob might even decide they want to retire earlier than age 65. Investing 30% of their money gives them something they otherwise wouldn’t really have: options.

Investing money gives you something you wouldn't otherwise have...options.

Ron Henry Click to Tweet

To recap, the steps are:

- Start investing 30% of income into Bucket 3. This step doesn’t stop until retirement.

- Use the remaining 5% to fill Bucket 1 which builds your emergency fund.

- Once the emergency fund is built, use the 5% to build Bucket 2. This also doesn’t stop until retirement.

The above arguments are why I feel a total savings rate of 35% is far superior and more practical than the conventional advice of 10%.

Pay Now or Pay Later

Achieving a 35% personal savings rate might not be easy at first. What I tell people is if living on 65% of your income doesn’t allow you to live the life you want now, then you need to come up with ways to increase your income. It’s a mindset shift that moves away from spending more of what you currently have to a mindset of growing your total income. 65% is the non-negotiable regular spending cap.

Add up what you spend for housing, food, clothing, and regular entertainment. Then compare that number to 65% of your current salary. If there’s a negative difference between the two, (and let’s face it, there probably will be), that number becomes the target for how much you need to increase your income. Focus on growth instead of scarcity.

It’s better to sacrifice now when you’re younger and have both the energy and desire to work hard. The last thing you want is to wake up one day in your golden years and realize that you would have been much better off had you hustled just a little bit harder when you were younger. If you can save 10% long term, you can save 35%. It’s all about goal-setting and mindset. When it comes to investing, time is your biggest asset. The sooner you begin, the more time you give the magic of compound interest to work its magic.

It Only Goes Right if it All Goes Right

Also consider that a 10% personal savings rate only works if everything works. Alice and Bob can’t have any major setbacks in their 35-year investing period. Neither can become unemployed, get sick, or need to take time off to care for a loved one. That’s quite a bet to make when the cost of getting it wrong is potentially running out of money when you’re older. It makes sense in life to continuously look for ways to increase your financial margin.

“It only goes right if it all goes right” is a financial bad plan because very few things in life always work out exactly as we expect them to. It’s a course of wisdom to plan for the worst while expecting the best. If you’re currently saving 10%, set the goal to increase it to 35% within the next 18 months.

"It only goes right if it all goes right” is a bad financial plan because very few things in life always work out exactly as we expect them to.

Ron Henry Click to Tweet

What are your thoughts? Is a 35% personal savings rate too aggressive? Let me know in the comments below!

A great FREE tool I personally use for tracking my portfolio is Personal Capital. When you click this link to sign up for your free account, both you and I will receive $20. Every little bit helps right?

Full Disclosure: The links on both the Essential Reading and my Books Reviews pages contain my Amazon affiliate code. If you purchase a book using that link I get a few pennies. Doing so does not change the price of the book for you.

Legal Disclaimer: The information provided and accompanying material is for informational purposes only. It should not be considered legal or financial advice. You should consult with an attorney, CPA or other professional to determine what may be best for your individual needs.