Sound financial decision making is a core requirement in achieving investing success. I was reviewing my articles on investing, goal achievement and avoiding financial mistakes and realized I that had not yet discussed financial decision making. Well today is the day. I have a few goals for this article.

The first is to define financial decision making. Next, we’ll discuss the areas of spending and investing since that’s where financial decision making has the most impact. We’ll talk about factors that negatively influence both activities. Finally, I’ll introduce a couple decision making models that I like. I suggest choosing a model that works for you and implementing it. A bonus to using decision making models is that they’re useful for areas of your life outside of managing your finances. Let’s get started.

Defining Financial Decision Making

Financial decision making is the process of weighing the pros and cons of a decision as it relates to the use of money. Sounds pretty simple right? In most cases, the health of your bank and investment accounts is a good indication as to whether or not you’ve been making good financial decisions. Extreme circumstances aside, long term wealth or poverty are most often byproducts of the decisions we make.

Like achieving anything of value in life, effective financial decision making starts with identifying goals. Goals drive plans. Plans produce intelligent action. Intelligent action over a period of time produces results.

Spending – Ask the Right Questions

As much as we’d like to think we always make rational decisions, this is hardly the case. As humans we’re largely emotional creatures. Learn to ask yourself “Why?” Why the new car, the house, that pair of Gucci shoes. Is the item an emotional fix for something else that’s going on in your life? Is the purchase a want or a need? There’s nothing wrong with buying things just because we want them but expensive “wants” should be tempered until you’re in a good financial position.

Be especially aware of who and what you allow to influence your financial decision making process. Is the purchase a case of you trying to keep up with the Joneses? Is TV advertising or seeing the cool things that your friends on social media are doing causing you to breaking out your credit card?

The Reality of Social Media

When it comes to public forums, people tend to only present the best sides of themselves. Don’t believe me? Get on your Facebook, Instagram or Snapchat account. Count how many pictures or posts there are of people looking depressed and not having the time of their life. I’d be willing to bet that you won’t find too many. Just like TV, what you see on social media is largely censored and/or fake. Oh, and the Joneses? They’re usually broke so it definitely wouldn’t be a good financial decision to imitate them. Competing with the highlight reel of another’s largely edited life is generally a bad idea. It’s a horrible idea in the area of finances.

A great rule I use for evaluating purchases in the “want” category is the 5X spending rule. To briefly summarize, it states that “if you can’t afford 5 of them, you can’t afford 1 of them”. I realize the rule sounds overly simple. But to quote Leonardo da Vinci, – “Simplicity is the ultimate sophistication.”

Resist the urge to spend real dollars to create a life that’s largely mythology. In day to day life, it’s much better to focus on creating systems to increase your financial margin. This usually results from consistently performing the same tasks, which can be seen as pretty boring. Maintaining focus of your long term goals should come before measuring up to an imaginary standard.

Investing

Much like spending, success as an investor lives or dies by good financial decision making. It starts with developing the emotional and psychological mindset of a successful investor. As I’ve repeated many times in my other articles, successful investing is more about managing yourself than managing money. The mechanics of investing is the easy part. Implementing those mechanics via unemotional financial decision making is often the primary difference between great and lackluster investment returns.

Said another way, the stock or mutual fund you pick is far less important than not doing silly things based on external influences.

Psychology

In my guide on getting started with stock market investing, I devote an entire section to understanding and developing your psychology. Two books I consider absolutely required reading are “What I Learned Losing A Million Dollars” and “Influence: The Psychology of Persuasion”. Both books are in-depth studies in the cognitive biases that can negatively affect good financial decision making. If you haven’t read them as yet, I highly recommend adding them to your reading list.

Running the Marathon

It’s helpful to view investing in the financial markets as a marathon instead of a sprint. Thinking in terms of 5 – 10-year periods will go a long way towards reducing your stress. An important aspect of good financial decision making is being able to filter information. Not all information is useful. In fact, I’d go so far to say that most of the financial-related information you encounter is actually detrimental to your decision making process.

“The price of oil is rising. The price of oil is falling. Company X missed their earnings by 3 cents. Company Y is in talks to acquire Company X. The Dow is down 1.2%. The Dow is up 1.5%”. In almost all situations this type of information is unimportant. It shouldn’t be the primary driver of your investment decisions. Don’t develop the habit of buying or selling based on someone else’s excitement. Realize that doing nothing is doing something and is often the course of good financial decision making.

Warren’s Thoughts on the Matter

In one of his letters to Berkshire shareholders Warren Buffett provided the following sage guidance:

“Inactivity strikes us as intelligent behavior. Neither we nor most business managers would dream of feverishly trading highly-profitable subsidiaries because a small move in the Federal Reserve’s discount rate was predicted or because some Wall Street pundit had reversed his views on the market. Why, then, should we behave differently with our minority positions in wonderful businesses? The art of investing in public companies successfully is little different from the art of successfully acquiring subsidiaries. In each case you simply want to acquire, at a sensible price, a business with excellent economics and able, honest management. Thereafter, you need only monitor whether these qualities are being preserved.”

In a nutshell, don’t allow others to do your thinking for you. Items 1 and 2 in my list of investing mistakes to avoid emphasizes this point. Perform your own analysis, develop a plan and stick to it. Even with great financial decision making, successful investing is a marathon, not a sprint. You don’t become wealthy in the stock market by constantly buying and selling positions. You become wealthy by sitting on your hands and letting the power of time and compound interest work their magic. If you fail to do this, the stock market will become a very expensive form of entertainment. That’s probably not the kind of entertainment you want.

Points to Ponder and the Superficial Knowledge Model

3 questions to ask yourself as you build your information filter could include:

- How does what I’m reading or hearing pertain to my documented investment approach?

- If I had not just heard or read “X” would I be buying or selling this position now?

- Am I allowing irrelevant facts to influence my financial decision making?

Answer them honestly each time you feel the need to do something with your investments.

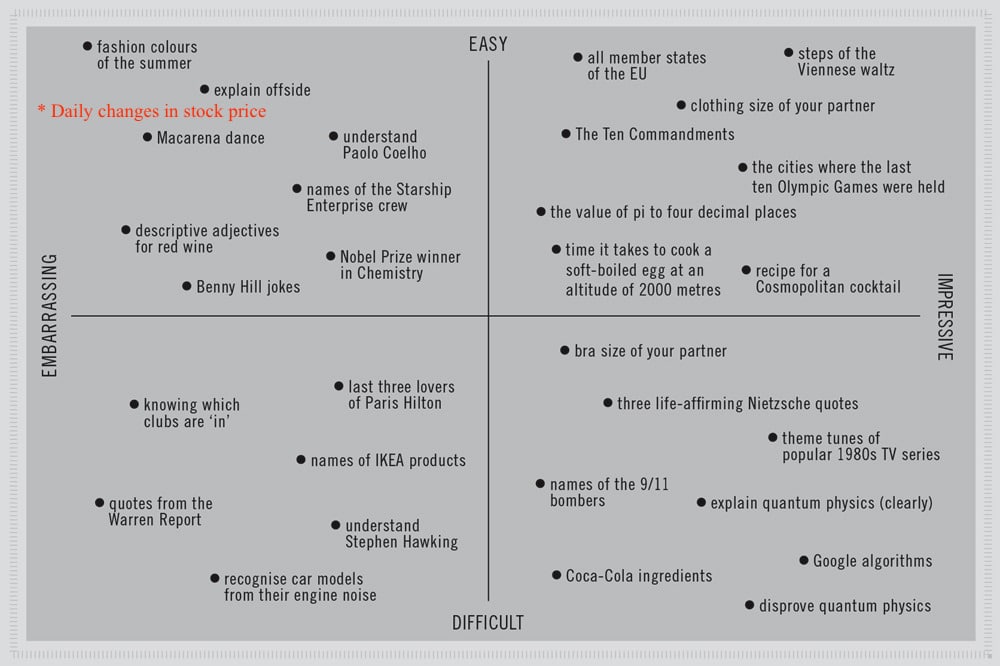

We’ll end this section with the introduction of superficial knowledge model. It was presented by the authors of The Decision Book as It’s a humorous way of displaying a matrix of information that although impressive, is largely unimportant. I added the day to day price of stocks to the upper left quadrant since having this information is both easy to obtain and embarrassing to classify as important. Take a look at what else made it into the model.

Superficial Knowledge Model

My Financial Decision Making Model

As we conclude our discussion on financial decision making, I’d like to talk about a model that I use daily in my financial decision making process. It allows me to prioritize how to best apply my efforts.

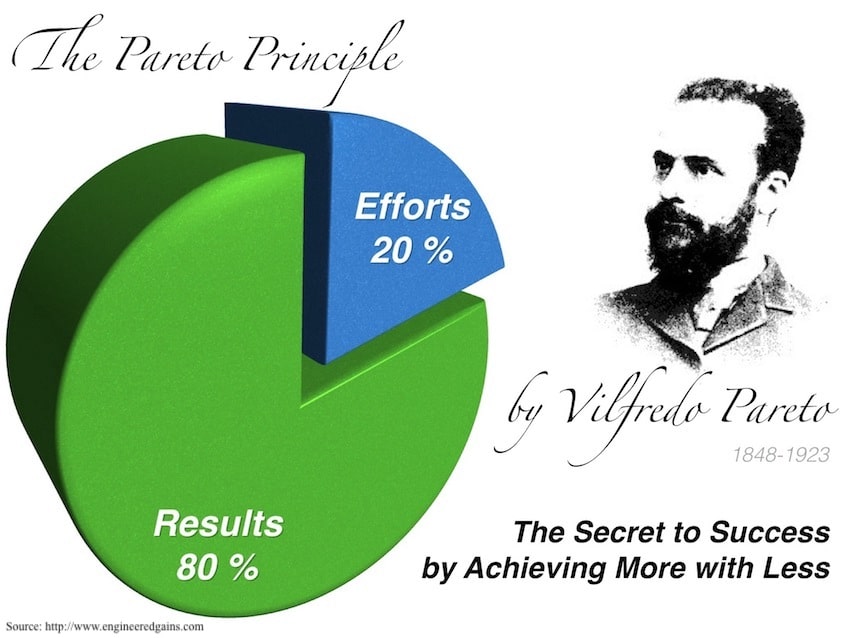

Prioritizing Effort – The Pareto Principle

At the start of the 20th century an Italian economist named Vilfredo Pareto observed that 80% of Italy’s wealth was controlled by 20% of the population. His finding that 20% of population command 80% of the influence was coined The Pareto Principal or the “80/20 rule”.

Vilfredo’s rule often extends to areas outside of wealth creation. 20% of the population commits 80% of crimes, 20% of people cause 80% of traffic accidents and so on. Take a look at your wardrobe closet. Would it be fairly accurate that you only wear 20% of your clothing 80% of the time? That one is especially true for me. Consider the place where you work. It’s not uncommon to find that most of the important work is done by only 20% of the employees. Weird but often very true.

80/20 Rule Application

So how can we use this model to improve our financial decision making? One great way is to recognize that 80% of our financial success is due to 20% of our spending and investment habits.

Spending

While small recurring expenses can impact our financial position, it’s those less common choices (the 20%) that make the biggest difference. For example, drinking designer coffee every morning can negatively impact your finances over a long period of time. That said, buying things like expensive cars, boats, and houses have a much larger financial impact. One choice (expensive coffee) can be likened to a death by 1000 cuts, while others (cars, boats, houses, other expensive habits) can be the equivalent of a financial guillotine.

Coffee, streaming services, and eating out are 80% purchases that have relatively low financial impact. Expensive toys, expensive habits and houses (20% purchases) are acquired far less frequently and yet have the largest financial impact. Now before you send me hate in the comments, let me state that I enjoy a good latte and I’m very much a car fanatic. I simply used coffee and cars as examples to make a point. It is important to recognize the roles each purchase plays in the big picture of your financial situation. Also, realize that some things, like eating out, can easily translate into large expensive habits, leading to some blurring of the lines between the 80% and the 20%.

To recap:

- 80% of our purchases create 20% of the financial impact (Coffee, Streaming Services, Eating Out, etc.)

- The remaining 20% of our purchases create 80% of the financial impact (Cars, Boats, Houses, etc.)

Spend more time scrutinizing that 20% purchase bucket. Controlling expenditures in this area contributes the most towards quickly improving your financial position.

Investing

In the investing world, the Pareto Principal applies as well. When you divide successful investing into its most basic parts it really boils down to 2 things: Security analysis and unemotional decision making. Those 2 make up the 20%. Conversely, reading every article in the Wall Street Journal, following the advice on CNBC, and staring at the stock ticker hourly all fall squarely into the 80% category.

I’m not saying that it’s not valuable to know what is regularly happening in the financial markets. The point I’m trying to make is that those activities don’t contribute to long term investing success as much as we’d like to think. With index funds being such a relatively low-risk way of entering the stock market, there’s really not a lot of analysis required for investors that take a long term approach. That part of the investing 20% is fairly easy. What remains is learning to manage your emotions.

Focus on the 20% that truly improves your financial decision making. That 20% is responsible for the majority of your investing success and frees you to do other things with your time.

Tying it Together

The time spent to improve your financial decision making process will pay huge dividends over time. You’ll become an information filtering machine; having the ability to quickly decide what information is valuable towards achieving your goals vs. what should be discarded.

Making better spending decisions and growing your investment portfolio will become byproducts of this effort. Don’t be quick to discount the importance of understanding and improving your psychology as part of this process. As tempting as it might be to skip ahead to investing, I feel this would be a mistake. Good financial decision making is built from the ground up.

The 2 books I recommended earlier (“What I Learned Losing A Million Dollars” and “Influence: The Psychology of Persuasion”) lay an excellent foundation for this process. Once you finish them, you’ll be in a better position to decide what additional knowledge you need to complete your personal decision making matrix.

What do you think? Are there other areas outside of spending and investing where you would benefit from applying the Superficial Knowledge and Pareto Principal models? Let me know in the comments below!

A great FREE tool I personally use for tracking my portfolio is Personal Capital. When you click this link to sign up for your free account, both you and I will receive $20. Every little bit helps right?