A huge part of building your personal money machine is having enough free cash to feed it. Investing requires money and the best way to know where your money is going is create a monthly budget. Yeah, yeah, I know. The “budget”. That dreaded “B” word that ruins all our spending fun. Even though they’re not the most fun thing to do for most people, that doesn’t mean you should ignore creating one. In order to manage money, you have to keep track of where it’s going.

I have great news though. Creating a monthly budget isn’t nearly as bad as you might think. I’ll show you how you can spend less than 15 minutes per month to create an effective budget. I can sense your excitement. There’s one topic we need to cover before digging into the black magic art of budget creation. It plays a huge role in how effective your budget will be long term. Let’s get to it.

Even though budgets aren't the most fun thing to do for most people, that doesn’t mean you should ignore creating one.

Ron Henry Click to Tweet

Budget Considerations for Single and Married People

Are you single or married? The answer to this question is important to our discussion. It dictates whether you’ll need to involve anyone else.

If you’re married and don’t involve your spouse in creating a monthly budget, chaos is going to ensue. Without fail you’ll either allocate too much or too little to a category they feel strongly about. Arguments and feelings of resentment are usually the result. To prevent this from happening you must have them be part of the process. You can be the one that actually tracks the spreadsheet, website or notepad, but they need to have a say.

Like most things in marriage, budget decisions shouldn’t be made unilaterally. I can’t stress how important this is.

If you’re single, it’s easy. You’re the captain of your ship so you get to decide how much to allocate to each category. It’s probably a good idea to have a close friend act as your accountability partner.

With the disclaimers out of the way, let’s move on.

If you’re married and don’t involve your spouse in creating a monthly budget, chaos is going to ensue.

Ron Henry Click to Tweet

Budget Tracking Options

You can use anything from a simple notepad to online software to create your monthly budget. I personally make use of a notepad because I enjoy the process of writing things out. When I actually write it down, it feels more real and, in my mind, represents an actual commitment. By notepad, I mean an actual notepad; not the application.

Budget Tracking Tool 1.0

Online Budgeting Tools

There are many options for tracking your money online with pros and cons to all of them. Let’s look at 7 of the more popular online budgeting tools.

Mint

Founded in 2006, Mint.com is one of the trailblazers in the online budgeting space. You’re able to connect your checking, savings, and credit card accounts to your Mint. This allows them to automatically import your transactions and assign tags in various categories like food, gas, utilities.

This tagging feature makes it very easy to visualize what you’re spending your money on. Mint allows for report generation complete with graphs that you can export. It’s a complete budgeting tool. Mint also offers a mobile application allowing you to keep track of your spending while on the go.

Personal Capital

Personal Capital is a complete wealth management tool. You can add your bank and investment accounts resulting in a complete financial picture. In addition to tracking your spending each month, the tool allows you to view if you’re on track to reach your retirement goals.

There’s an investment tracker which allows you to view the performance of all your investments individually or combined. You’re also able to compare their performance against benchmarks like the S&P 500, US Bonds, the Dow and Foreign markets. Personal Capital is the money management tool that I personally use. The features are incredible and it’s absolutely free. For a complete walkthrough of the Personal Capital interface and its features, check out my review.

EveryDollar

EveryDollar is a newer budgeting tool created by the team at Dave Ramsey. It offers an easy way to implement a zero-sum budget. If you’ve ever listened to Dave or read any of his books, you know he’s all about making every dollar work as hard as possible.

There’s a paid and free version of this application. The Plus version allows you to automatically connect EveryDollar to your bank account. There’s a $99.00 annual cost for using the Plus version of the tool. This is a negative since most other popular budgeting tools like Mint and Personal Capital allow you to do this for free.

MoneyStrands

MoneyStrands is a budgeting tool that is completely free. You can connect your bank accounts, create spending plans and schedule upcoming bill payments. A pretty cool feature of MoneyStrands is its support for multiple languages and currencies.

Unlike the other tools mentioned so far, this tool is mobile only. Currently the only way to access it is using your iOS or Android device. This might be a deal-breaker for you if you prefer to use a full-featured computer.

BudgetPulse

BudgetPulse is a free online personal budgeting tool that offers the perfect combination of simplicity and functionality. It was designed so that anyone can quickly and easily take control of their personal finances.

Unlike the other tools mentioned so far, BudgetPulse is completely offline. BudgetPulse does not sync account information with your bank. This might be attractive to some who are wary of handing their account numbers and passwords over to an online application.

There are no downloads. No complicated software. In addition, by not requiring personal credit card or bank information, BudgetPulse effectively eliminates the risk of identity theft.

YNAB

You Need A Budget (YNAB) is a paid online budgeting tool that integrates with your bank for automatic transaction syncing. Some key features include a debt paydown tool, goal tracking and extensive reporting options.

YNAB is very forward-thinking in that they’ve created many options for getting the most out of the tool. There’s an online user forum, help documentation, weekly videos, podcasts and a newsletter. These options show the company’s extensive commitment to their users. They really want to be part of helping you realize your financial goals.

BudgetSimple

BudgetSimple is a budgeting tool that has a strong focus on debt reduction and meeting other financial goals. The free version allows you to create a budget, track spending and generate reports. The paid version will cost you $4.99 per month and adds integration with your bank and credit card accounts. You also get access to the mobile application when you opt for the paid version.

Even though it’s a newer offering the company definitely is confident in the paid version of their product.

“We guarantee you’ll save money and understand your finances better within the first hour of using BudgetSimple.”

I believe their claim. For most people, seeing where your money is going is usually an eye-opening experience. Although Mint and Personal Capital offer completely free software, you might opt for BudgetSimple if you’re looking for a tool focused on debt reduction.

Online Budgeting Tool Summary

As you can see, there are many options for online budgeting tools. The 7 above are among the most popular. With the tools out of the way, onto actually creating our monthly budget!

Guidelines for Creating A Monthly Budget

I sub-divide my monthly budget by paycheck. Since I get paid bi-weekly, I’ll have a sub-section titled with the date and amount of each paycheck. I then place the expenses under each paycheck depending on when they’re due throughout the month.

In the situations where your income is irregular, I’d recommend averaging income over the past 3 months. This will allow you to come up with an income number to use in your budget.

Irregular Expenses

If you’re like me, you’ll likely have expenses like auto insurance, home insurance and professional membership fees. Most bills of this type offer a substantial savings if they’re paid on an annual or semi-annual basis.

If you choose to take advantage of the discount, simply divide the total premium by 12 to come up with the amount you need to set aside each month. Whatever that number is, I would add 10% so you have some wiggle room for future rate increases. It’s not like these things get cheaper over time right?

Irregular Expense Budgeting Example:

Let’s say your annual auto insurance costs $1,440.00. We’ll take that amount and divide it by 12 to come up with $120.00. Next , let’s add 10% to the monthly cost to arrive at $132.00. This is the number I would use in your budget. That extra $12.00 per month slightly increases your financial margin. If the cost of your insurance rises, you’re covered. If not, you can either save the money or use it to increase your investments.

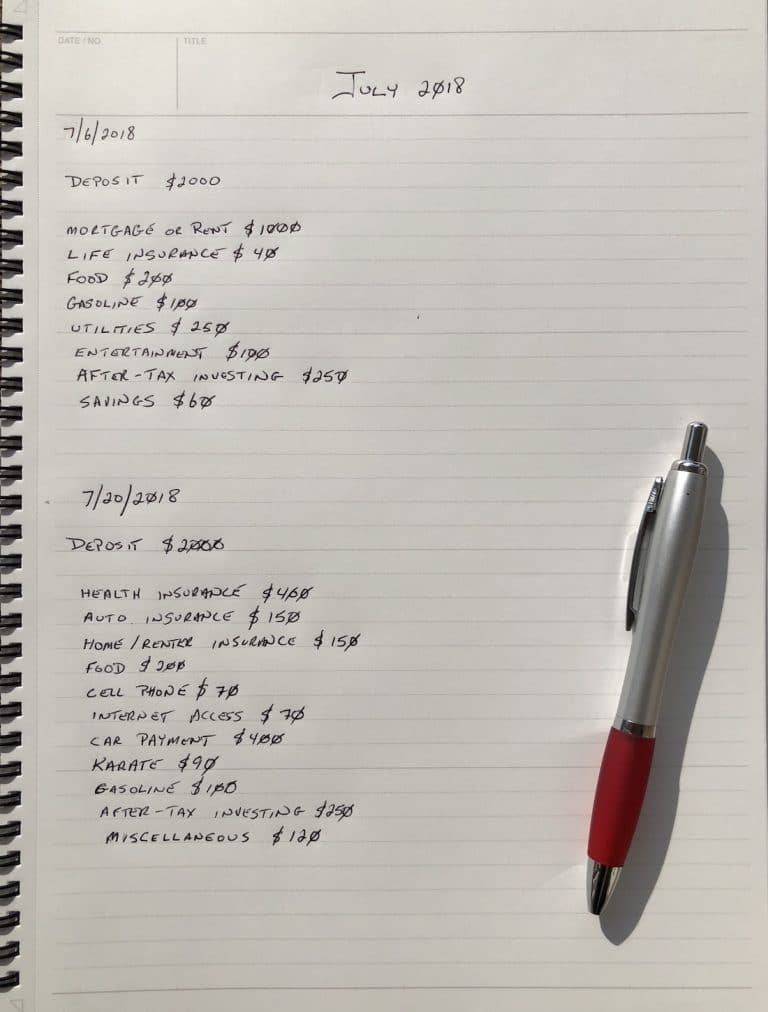

Monthly Budget Example

I’ve created a fictional budget to serve as an example. I based the income amount on a salary of approximately $65,000 per year. Creating a monthly budget is a very personal thing and has to fit what you have going on your life. Not everyone will have a car payment or mortgage. Some people will have credit card debt or student loans in their budget.

You also might not be subject to utilities such as electricity, gas and water. There are living situations (college students and some apartments) where they are included, so I went with a relatively low amount to cover them. Depending on your situation, you’ll have to add/remove items as you see fit.

My example is just to give you some ideas of how you can create your budget.

Creating a monthly budget is a very personal thing and has to fit what you have going on your life.

Ron Henry Click to Tweet

You’ll notice I pay different expenses at different times of the month. Other than the $120 “miscellaneous” category in the second pay period, every dollar that comes in is earmarked for something. I think this is an important habit to develop. You want to eventually get to the point where the “miscellaneous” category is a very small percentage of your income. This will happen over time as you get better at estimating your expenses.

You probably also noted that a substantial portion of income is allocated towards investing and savings. You might not be able to reach these numbers at first but they represent a good goal. Investing is important for building long term wealth and financial security over time.

Concluding Thoughts

Once created, you might be tempted to simply transfer the same budget to every month. I’d highly discourage you from doing this.

At the beginning of every month, take note of what could be unique. Do you have an upcoming vacation planned? If so, add the costs associated with it to your budget. Perhaps you’re planning on replacing some clothing or doing home upgrades. Again, those types of things should be accounted for.

Rather than viewing your budget as this rigid never-changing document, take a different approach. View it as the money management tool of your life. Just like life, there are ebbs and flows every month. Like life, your budget is a living document that should monthly reflect whatever is going on in your financial world.

Like life, your budget is a living document that should monthly reflect whatever is going on in your financial world.

Ron Henry Click to Tweet

It Takes Time to Get Right

It’s important to remember that like most things, you’re probably not going to do the best job at first. It’s not usually until month 3 or 4 that most people get a handle on creating a monthly budget that accurately reflects reality. Don’t get discouraged when you’re starting out. Stick with it. You’ll get better over time. Eventually you’ll be able to complete your monthly budget meeting in under 15 minutes.

I hope you found this useful. Did you pick up any good ideas for creating your budget? Are you going to use the “pen and pad” method or will you opt for one of the online tools? Let me know in the comments below!

A great FREE tool I personally use for tracking my portfolio is Personal Capital. When you click this link to sign up for your free account, both you and I will receive $20. Every little bit helps right?